Variable interest rate on a line of credit for home equity

A home equity line credit is a great option to borrow against your home equity. This can also make it a valuable tool for large projects. However, this can be risky if interest rate fluctuations are high. It is important to understand the difference between a fixed-rate and variable-rate HELOC. A fixed-rate HELOC can be fixed for a set period of time such as 10 years. Variable-rate HELOCs allow you to borrow unlimited amounts of money.

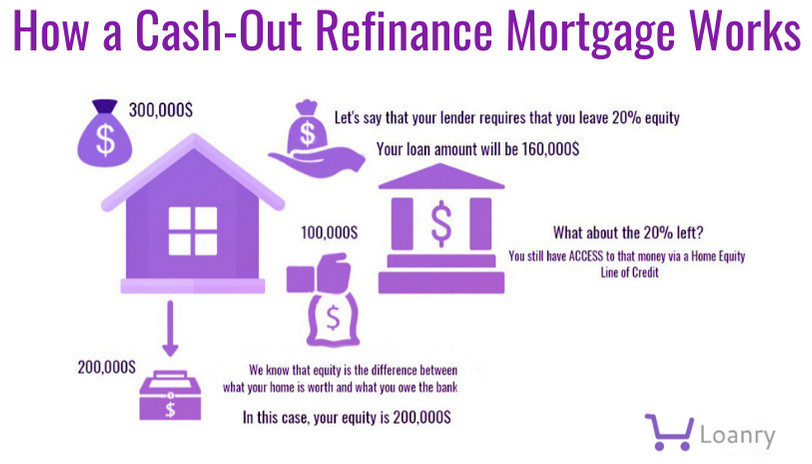

There are many factors that affect how much you can borrow on a line of credit for home equity. An easy calculation will give you an estimate of the maximum amount you can borrow.

Fixed-rate loans secured by your home

A fixed-rate, secured loan secured by your property may be possible if you have equity in your home. This loan is perfect for someone who has a clear idea of how much money they require and needs a lump sum. They can use the money to pay for any purpose, including home improvement. You can also deduct the interest on your income taxes

Fixed-rate home equity loans are secured with your home's equity. The rate of the loan is tied to an independent benchmark like the U.S. Prime Rat, currently 3.5 per cent. Most lenders require a minimum credit score of 620, but some have higher minimums. As a rule, a higher credit score will help you get a lower interest rate.

Maximum amount of loan you can get

You can borrow up to 80 percent of the equity in your home with a home equity loan. This amount is also known as the maximum amount you can borrow with a home equity line of credit (HELOC). This type loan allows you to make improvements to your home to increase its value. But before you borrow against your home, here are some points to remember.

First, consider your income and credit scores. These will affect how much you are able to borrow. A home equity loan may not be possible if your income is too low. Additionally, home equity loans may carry high upfront fees. These fees may reduce your maximum loan amount.

There are some downsides to a loan for home equity

A home equity loan might be an option if you want to borrow money against the property's value. The benefit of home equity loans is that you don't have to put your home at risk. You should still be able to repay the money borrowed. The best way to prepare is by keeping an accurate record of your income and expenses. This way, you can make sure that you can afford the new payment you'll have. While the process of applying for a home equity loan is fast, it's not a guarantee that you'll be approved for it.

Home equity loans have another advantage: the interest rate is lower that many other financial products. While the interest rate will depend on your creditworthiness it is usually lower than a creditcard or an unsecured personal loans. A home equity loan can also be tax-deductible. A home equity loan may be able to lower your tax bill depending on your credit score. A home equity loan is able to be reinvested in your home, unlike a personal loan or credit card.

FAQ

What is the maximum number of times I can refinance my mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. You can refinance in either of these cases once every five-year.

What should you think about when investing in real property?

It is important to ensure that you have enough money in order to invest your money in real estate. You will need to borrow money from a bank if you don’t have enough cash. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

You also need to make sure that you know how much you can spend on an investment property each month. This amount should include mortgage payments, taxes, insurance and maintenance costs.

Finally, ensure the safety of your area before you buy an investment property. It would be a good idea to live somewhere else while looking for properties.

What should I do if I want to use a mortgage broker

A mortgage broker can help you find a rate that is competitive if it is important to you. Brokers are able to work with multiple lenders and help you negotiate the best rate. Brokers may receive commissions from lenders. You should check out all the fees associated with a particular broker before signing up.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

The first step in moving to a new location is to find an apartment. This requires planning and research. This involves researching neighborhoods, looking at reviews and calling people. Although there are many ways to do it, some are easier than others. Before you rent an apartment, consider these steps.

-

Data can be collected offline or online for research into neighborhoods. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Other sources of information include local newspapers, landlords, agents in real estate, friends, neighbors and social media.

-

Find out what other people think about the area. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You can also check out the local library and read articles in local newspapers.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what they loved and disliked about the area. Ask them if they have any recommendations on good places to live.

-

Be aware of the rent rates in the areas where you are most interested. If you think you'll spend most of your money on food, consider renting somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out about the apartment complex you'd like to move in. What size is it? How much does it cost? Is the facility pet-friendly? What amenities are there? Are there parking restrictions? Do tenants have to follow any rules?