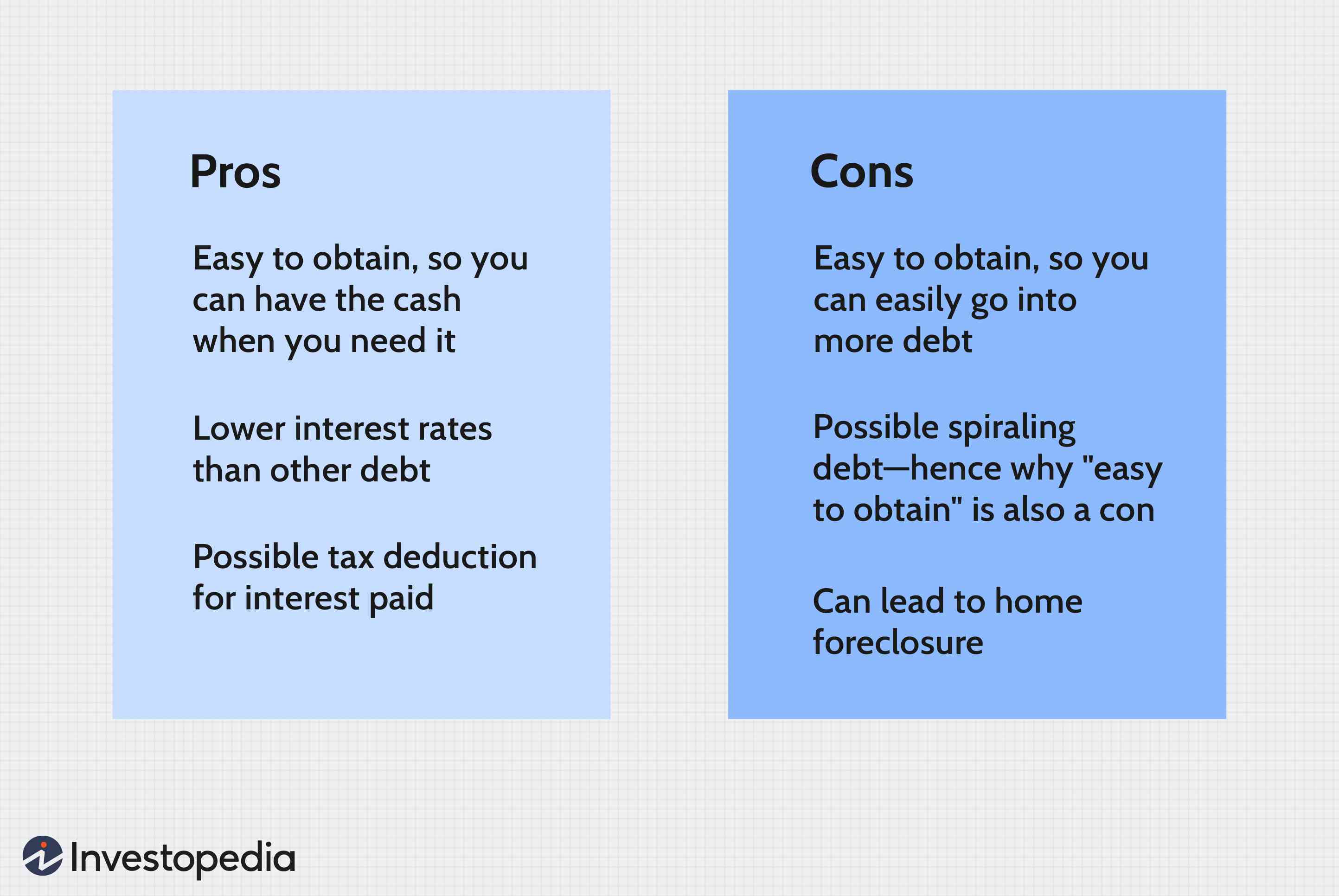

A Home equity card (HELOC) can be linked to the equity in your property. This is a great option for elderly homeowners, and it can be used to consolidate your debt. However, there are some cons. These are some of the cons and pros to this credit card.

Home equity line-of credit

Home equity lines can be secured by equity in your home. They can be a valuable financial tool for homeowners. The lender will allow you to borrow as much as 60% or as much 85% of your equity. These loans have some disadvantages, such as lower interest rates and flexibility.

Although a home equity loan is an option that can provide financial security, there are some things you need to be aware of. It is a loan and you will have to pay interest immediately. If you don't use the funds for a specified period of time, some lenders may charge an inactivity fee.

It's a credit-card that's tied to the equity of your home.

HELOCs are revolving credit lines similar to credit cards that are tied to equity in your home. It can be used to make large purchases or pay off higher-interest debt. You can borrow up to the amount that you have. This credit type is typically lower than those for other types of loans. It may also be tax deductible.

HELOCs can be used to make major purchases or to fund a vacation. You can also use your HELOC to reduce high interest debt, pay for a vehicle or for other unexpected expenses. However, you must remember that the credit line is tied to your home's equity, and you should only use it for major purchases. Lenders will assess you ability to pay the credit line and your other financial obligations.

This is a good choice for older homeowners

A HELOC, or revolving loan of credit, is a revolving form of credit. This loan allows older homeowners to borrow money with no down payment. These loans can be secured by the equity of the homeowner. Lenders can take over the home if you are unable to pay the loan payments on time. HELOCs can also help finance education expenses for your children and grandchildren. It can be used for home improvements, or to pay medical bills.

HELOCs also have a low interest rate. They are far less expensive than reverse mortgages and offer more flexibility. However, there are some downsides.

It can also be used to consolidate your debt.

A HELOC, or High-End Loan on Credit, is a great option to consolidate and simplify your financial situation. Not only can you combine all of your debt, but you can also reduce the amount of interest you're paying on each account. HELOCs are typically lower than secured personal loans and credit cards. Citizens provides two repayment options and support throughout the entire process. This loan allows you to use the equity in your home to pay off your high interest debt.

HELOCs allow you to pay down high-interest credit card balances. A HELOC is more flexible than a card because it has a longer repayment period. You can make additional payments towards the principal balance of your HELOC to reduce your interest payments. Another advantage of using a HELOC to consolidate debt is that it improves your credit score.

It can also be used to purchase a new home.

You only pay interest when you use your HELOC for a second residence. HELOCs have a lot of flexibility which makes them attractive. You can use the equity in your home to pay down your debt, and the income from the investment property can help offset the debt. If your income is sufficient to cover the mortgage payment, you might be able to buy a second home using the income it generates. However, you should be aware that you will be exposed to changes in the housing market.

If you plan to buy a second home, you may need some extra capital to pay off the down payment and other expenses. HELOCs can be used to offset equity that you have already built in your current home. If your home is still for sale, however, you won't be eligible to get a HELOC.

FAQ

What is a reverse loan?

Reverse mortgages are a way to borrow funds from your home, without having any equity. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers your repayments.

What are the key factors to consider when you invest in real estate?

The first step is to make sure you have enough money to buy real estate. You can borrow money from a bank or financial institution if you don't have enough money. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

It is also important to know how much money you can afford each month for an investment property. This amount should cover all costs associated with the property, such as mortgage payments and insurance.

Finally, ensure the safety of your area before you buy an investment property. It would be a good idea to live somewhere else while looking for properties.

What should you look for in an agent who is a mortgage lender?

A mortgage broker helps people who don't qualify for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge fees for this service. Some brokers offer services for free.

How do I eliminate termites and other pests?

Your home will be destroyed by termites and other pests over time. They can cause serious damage to wood structures like decks or furniture. To prevent this from happening, make sure to hire a professional pest control company to inspect your home regularly.

Do I need flood insurance

Flood Insurance covers flood damage. Flood insurance protects your belongings and helps you to pay your mortgage. Learn more about flood coverage here.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

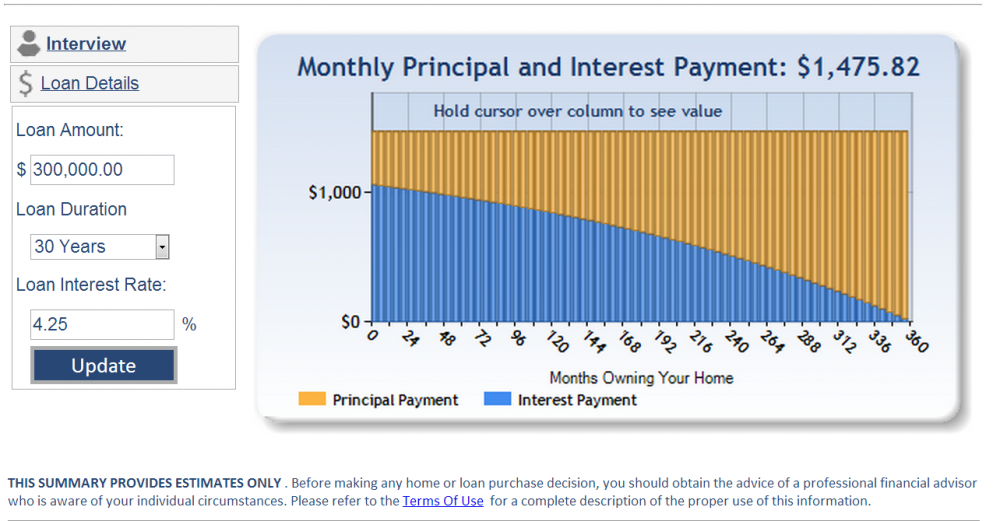

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How do you find an apartment?

When moving to a new area, the first step is finding an apartment. This takes planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. There are many ways to do this, but some are easier than others. Before renting an apartment, it is important to consider the following.

-

Data can be collected offline or online for research into neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

See reviews about the place you are interested in moving to. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. Local newspaper articles can be found in the library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them about what they liked or didn't like about the area. Also, ask if anyone has any recommendations for good places to live.

-

Consider the rent prices in the areas you're interested in. You might consider renting somewhere more affordable if you anticipate spending most of your money on food. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out information about the apartment block you would like to move into. Is it large? What is the cost of it? Is it pet friendly? What amenities are there? Is it possible to park close by? Are there any special rules for tenants?