A down payment calculator allows buyers to calculate how much money is needed for a downpayment on a home. This calculator lets you input the price of the house, the downpayment percentage, and the monthly rent payment to calculate the downpayment percentage. Once a buyer has an idea of how much money they will need, they can use a down payment calculator to come up with a budget.

Renter budget equivalent calculator

Calculating your mortgage affordability is important if you are renting and looking to purchase a home. A renter budget equivalent downpayment calculator can be used to determine whether you can afford a mortgage. It is based on your current rent costs. You can enter your current rent payment as well as future mortgage payments. The calculator allows you to input property taxes as well as annual insurance costs.

If your income is greater than average, rent can be afforded up to 40%. You'll be able to live in a larger space and have a better location. You will need to carefully monitor your spending and decide if you can afford to pay more. Also, be sure to assess your financial situation prior to signing a lease.

Cost of mortgage insurance

The best way to calculate the cost for mortgage insurance is to use a down payment calculator. This insurance is typically paid by the borrower and is based on their FICO credit score. Before deciding how much mortgage coverage a borrower must have, mortgage lenders take several factors into account. A borrower with a small downpayment may not need mortgage insurance.

Different insurers charge different rates for PMI. This means that a borrower could find a lower rate or a higher rate by shopping around. Costs will vary depending on the amount of the loan, as well as the discretion of the lender. Before choosing a PMI program, it is best that you speak to an experienced loan officer.

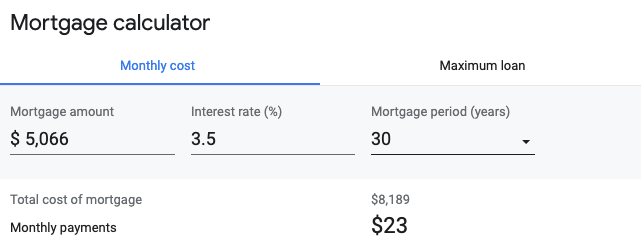

Amount of down payment

A down payment calculator is a valuable tool that helps you calculate the amount of down payment you should make on a house. Because borrowers with longer repayment terms are likely to pay less interest, larger down payments can be more beneficial. A large downpayment can make it difficult to sell or refinance the property.

The calculator will let you enter the price for the home you wish to buy, and then calculate how much money it will cost you to save. You can specify a price or a percentage.

Taxes

Using a down payment calculator is essential when considering the cost of a home purchase. A down payment, unlike a credit card payment, is the only upfront payment during the home buying process. Other costs include points on your loan, insurance, lender title insurance, survey fees, inspection, appraisal and insurance. These costs could add up to three percent to the purchase price.

PMI

Many homebuyers find it difficult to save up 20% for their down payment. PMI loans allow them to buy a house with a lower downpayment and then cancel the loan when they have 20% equity. Based on your credit score as well as the down payment amount, PMI can range between 0.3% and 1.5%. In some cases, you can request that your lender cancel PMI after you have built up more than 20% equity.

PMI is usually paid at closing or as a monthly fee. However, you can also choose to pay it upfront. A PMI-down payment calculator and a PMI calculator are useful tools to determine the amount that you need to deposit as well an amortization plan. A mortgage insurance calculator does not replace professional advice. Consult a loan officer for further information and advice.

FAQ

What are the chances of me getting a second mortgage.

Yes. However it is best to seek the advice of a professional to determine if you should apply. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What are some of the disadvantages of a fixed mortgage rate?

Fixed-rate mortgages tend to have higher initial costs than adjustable rate mortgages. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

How much does it take to replace windows?

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

How can I fix my roof

Roofs can leak because of wear and tear, poor maintenance, or weather problems. Repairs and replacements of minor nature can be made by roofing contractors. Get in touch with us to learn more.

How long does it take for my house to be sold?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It can take from 7 days up to 90 days depending on these variables.

How long does it usually take to get your mortgage approved?

It is dependent on many factors, such as your credit score and income level. It typically takes 30 days for a mortgage to be approved.

Should I use a broker to help me with my mortgage?

A mortgage broker can help you find a rate that is competitive if it is important to you. A broker works with multiple lenders to negotiate your behalf. Some brokers receive a commission from lenders. Before you sign up, be sure to review all fees associated.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

Finding an apartment is the first step when moving into a new city. This involves planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. This can be done in many ways, but some are more straightforward than others. The following steps should be considered before renting an apartment.

-

You can gather data offline as well as online to research your neighborhood. Online resources include Yelp. Zillow. Trulia. Realtor.com. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

Review the area where you would like to live. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what the best and worst things about the area. Ask them if they have any recommendations on good places to live.

-

Take into account the rent prices in areas you are interested in. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. However, if you intend to spend a lot of money on entertainment then it might be worth considering living in a more costly location.

-

Find out all you need to know about the apartment complex where you want to live. Is it large? How much is it worth? Is it pet-friendly What amenities do they offer? Can you park near it or do you need to have parking? Are there any rules for tenants?