Low LTV mortgages are a great choice for people who want to avoid private mortgage insurance or other costs. This can allow for more flexibility in loan programs and faster approvals. The best part is that you can obtain a low LTV home loan by making creative arrangements. For example, you could bring in a larger down payment with a coborrower or split the financing into 2 loans.

Maximum 80% loan to value

A low loan-to value mortgage at 80% may be an option for those who don’t have the funds to pay a large downpayment. Mortgage insurance can be costly so borrowers are able to avoid a mortgage with a low LTV limit. It can also improve your chances of qualifying for your preferred loan option. It can also help you save thousands of dollars every month on your monthly payment.

A high loan/to-value ratio can lead to higher mortgage interest rates and increased mortgage insurance. In these situations, it may be worth taking a step back and saving up for a larger down payment.

Combination mortgages

Combination low LTV Mortgages are a great option to help you get into a home. These loans require less than 20% down, and you can often get approved for less than 80% LTV. You may also be able to avoid paying PMI.

However, combination loans usually have higher interest rates that other mortgages. The combination loan may be a good option for you if your budget allows. You should know that a second loan at a higher interest rate will result in higher monthly payments and require more upfront money. This means that you should weigh the costs and benefits of multiple loans before choosing which option to pursue.

Repayment mortgages

People who can't afford higher down payments may consider low LTV mortgages. These mortgages will reduce the total amount of your loan by requiring that you pay less than your home's or car's market value. A higher down payment may be able to help you afford a low LTV. To determine the impact on your monthly mortgage payments, use a mortgage calculator.

Mortgages with low LTV repayments tend to be cheaper than those with high LTV. Lenders view borrowers with high LTV as risky, so they will charge higher interest rates. Whether your LTV is 70%, 60%, or even more, the interest rate will depend on a number of factors, including market conditions, competition among lenders, and the Bank of England interest rate.

Criteria for a low ltv loan

There are several factors that must be considered when applying for a low LTV mortgage. LTV of a property is the amount of the property that is being funded. Ninety percent is the maximum LTV that can be allowed in most cases. There are exceptions. A mortgage with a low LTV will generally require a smaller downpayment.

LTV that is lower means lower monthly mortgage payment. This could save you thousands of dollars over the life of your loan. 80% is a common LTV, and a 20% down payment can provide that ratio.

FAQ

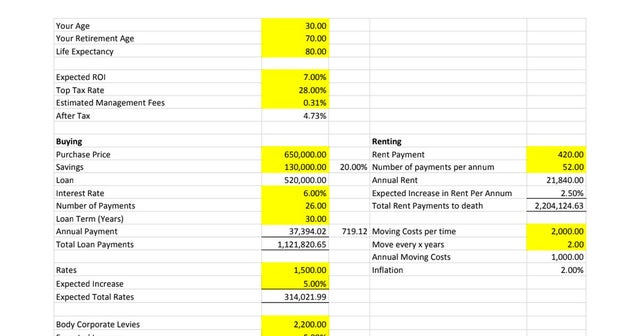

Is it better to buy or rent?

Renting is usually cheaper than buying a house. But, it's important to understand that you'll have to pay for additional expenses like utilities, repairs, and maintenance. There are many benefits to buying a home. You will be able to have greater control over your life.

Do I need a mortgage broker?

A mortgage broker may be able to help you get a lower rate. A broker works with multiple lenders to negotiate your behalf. However, some brokers take a commission from the lenders. Before you sign up for a broker, make sure to check all fees.

What flood insurance do I need?

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings and your mortgage payments. Find out more information on flood insurance.

What is a Reverse Mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. You can draw money from your home equity, while you live in the property. There are two types: government-insured and conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. FHA insurance will cover the repayment.

How many times do I have to refinance my loan?

This depends on whether you are refinancing with another lender or using a mortgage broker. In both cases, you can usually refinance every five years.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How do I find an apartment?

Moving to a new place is only the beginning. Planning and research are necessary for this process. This involves researching and planning for the best neighborhood. This can be done in many ways, but some are more straightforward than others. The following steps should be considered before renting an apartment.

-

Online and offline data are both required for researching neighborhoods. Online resources include Yelp and Zillow as well as Trulia and Realtor.com. Offline sources include local newspapers, real estate agents, landlords, friends, neighbors, and social media.

-

Find out what other people think about the area. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also find local newspapers and visit your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them about their experiences with the area. Ask for recommendations of good places to stay.

-

Consider the rent prices in the areas you're interested in. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out information about the apartment block you would like to move into. Is it large? What is the cost of it? Is it pet friendly? What amenities do they offer? Are there parking restrictions? Do tenants have to follow any rules?