If you plan to live in your home for many years, paying upfront PMI can be a great option. This is because the upfront premium can be used to increase your downpayment and home equity. It is also possible to refinance your loan so that you no longer have to pay the insurance monthly. Be aware of the potential costs before you make a decision. Paying PMI upfront can have a significant impact on your monthly mortgage payments, so make sure you consider all your options before deciding.

Alternatives to paying PMI upfront

There are many options available to you if you want to save money on your mortgage. PMI can either be avoided through refinancing or you can pay for your mortgage insurance. However, these options come with limitations. You may also have to pay a higher mortgage rate. Also, these options do not eliminate PMI like the traditional type.

The PMI concept is not for everyone. However, it's more cost-effective than other loan options. You could save hundreds of thousands by asking your lender for a PMI Loan. Here are some of these options: One of the best ways to avoid paying PMI is to have a larger down payment. This will allow you to save money and negotiate a lower final sale price with your seller.

A monthly premium plan is another option. This plan is for borrowers with extra cash or who want to reduce their housing costs. The monthly premium will depend on the loan amount. You can also opt to pay one premium upfront.

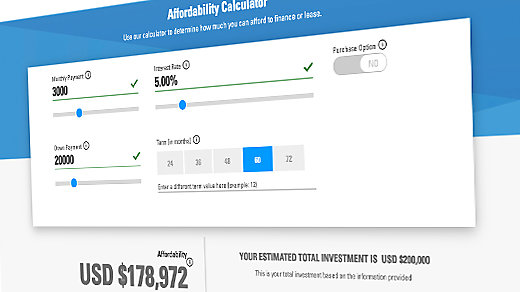

Calculating your PMI payout

You will need to consider your credit score, loan-to-value ratio and other factors when determining your PMI payment. These factors are taken into consideration to help you estimate your monthly payments. Also, consider how much down payment you are willing to make. In some cases, a lower downpayment might help reduce your PMI premiums.

PMI can either be paid monthly or as a one time payment depending on which type of mortgage you have. Because it doesn't require upfront payments, the latter is more popular. You should know that the monthly payment will likely be higher as a result.

PMI is an additional cost but can have significant benefits for long-term wealth accumulation. It will help you build equity and get into your home faster. However, it's important to keep in mind that you'll need to pay at least as much PMI as the price of the home itself.

Refinance your loan in order to eliminate PMI

PMI is private mortgage insurance. A conventional mortgage with a down payment of less than 20% will likely result in you paying PMI. Refinancing a loan can remove PMI if the loan balance is more than 80%. This will allow you to lower your monthly payments, but preserve as much of your equity as possible.

PMI costs can add hundreds of dollars each month to your monthly payments. Refinancing your loan to remove PMI can help you get rid of the expense and lower your monthly payment. Some homeowners are able to refinance into a loan without PMI, while others must refinance into a different loan. It is crucial to fully understand all requirements before you begin the process.

There are a few factors you should keep in mind when refinancing your loan to remove PMI. You need to determine how much money you would save versus how much you would pay back if you didn't refinance. The refinancing calculator helps you estimate how much money you can save on your loan to get rid of your PMI.

FAQ

What should you consider when investing in real estate?

The first thing to do is ensure you have enough money to invest in real estate. You will need to borrow money from a bank if you don’t have enough cash. You also need to ensure you are not going into debt because you cannot afford to pay back what you owe if you default on the loan.

You also need to make sure that you know how much you can spend on an investment property each month. This amount should cover all costs associated with the property, such as mortgage payments and insurance.

Finally, you must ensure that the area where you want to buy an investment property is safe. It would be best to look at properties while you are away.

How many times may I refinance my home mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. Refinances are usually allowed once every five years in both cases.

What are the chances of me getting a second mortgage.

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What are the pros and cons of a fixed-rate loan?

A fixed-rate mortgage locks in your interest rate for the term of the loan. You won't need to worry about rising interest rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

How much will my home cost?

It depends on many factors such as the condition of the home and how long it has been on the marketplace. Zillow.com says that the average selling cost for a US house is $203,000 This

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes are homes built on wheels that can be towed behind vehicles. Mobile homes have been around since World War II when soldiers who lost their homes in wartime used them. Today, mobile homes are also used by people who want to live out of town. These homes are available in many sizes and styles. Some are small, while others are large enough to hold several families. Some are made for pets only!

There are two types of mobile homes. The first is made in factories, where workers build them one by one. This is done before the product is delivered to the customer. Another option is to build your own mobile home yourself. First, you'll need to determine the size you would like and whether it should have electricity, plumbing or a stove. Next, make sure you have all the necessary materials to build your home. The permits will be required to build your new house.

Three things are important to remember when purchasing a mobile house. You may prefer a larger floor space as you won't always have access garage. You might also consider a larger living space if your intention is to move right away. You should also inspect the trailer. You could have problems down the road if you damage any parts of the frame.

Before buying a mobile home, you should know how much you can spend. It is important to compare prices across different models and manufacturers. Also, look at the condition of the trailers themselves. Many dealers offer financing options. However, interest rates vary greatly depending upon the lender.

An alternative to buying a mobile residence is renting one. Renting allows for you to test drive the model without having to commit. Renting isn’t cheap. Most renters pay around $300 per month.